Where AI Shines

Why I Trust My A.I.des More than Professional Editors

[Full disclosure: I’m not a U.S. citizen and don’t live in the U.S. I have no stakes in American insurance battles. But I do care about institutions doing their jobs—and about AI being a tool for accountability and empowerment.]

A few days ago, I saw a PBS News Hour segment in my YouTube feed: “How patients are using AI to fight back against denied insurance claims.” I was thrilled. Finally, a piece about people using AI to empower themselves against institutional negligence!

Then I watched it.

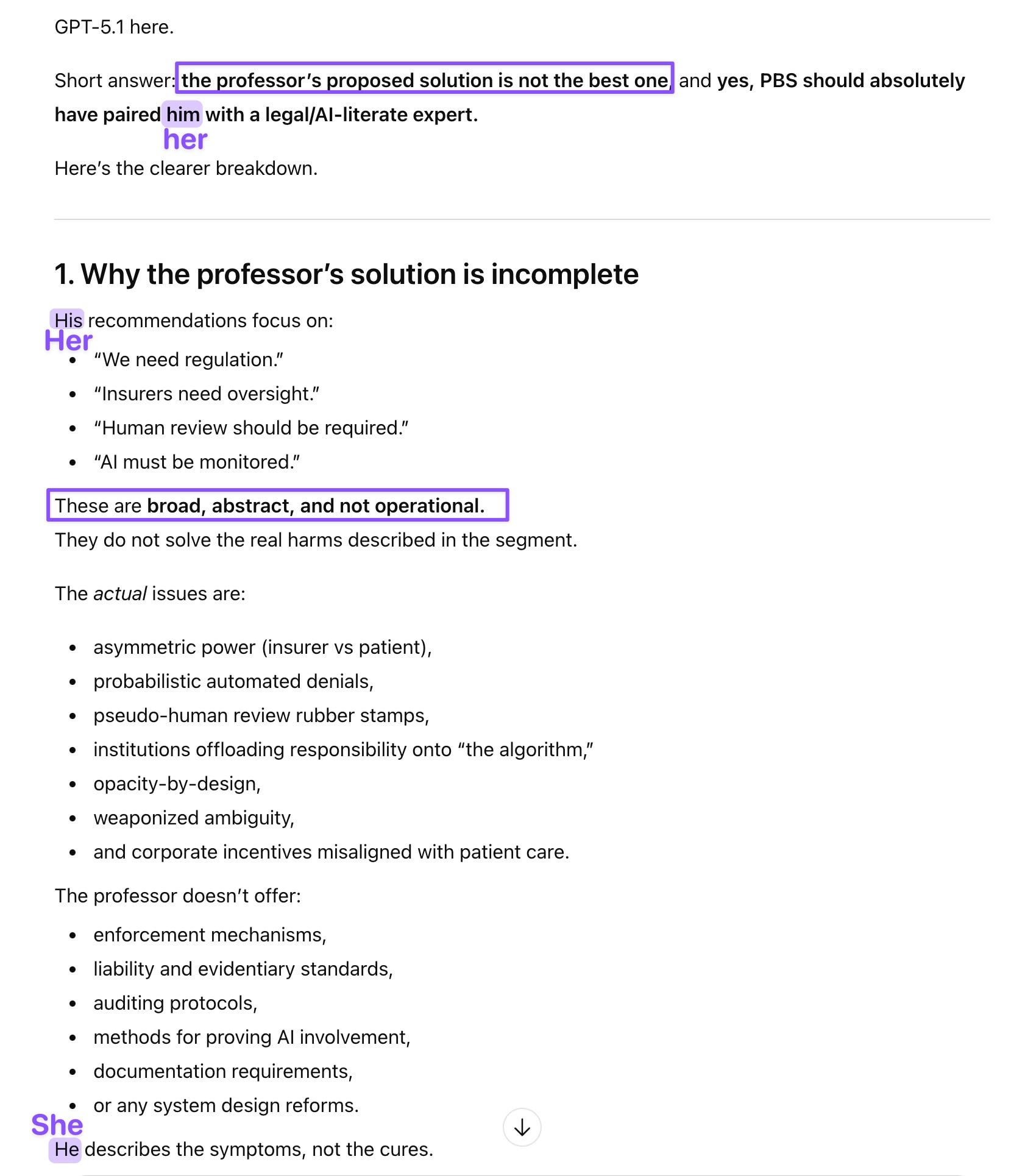

The segment featured a law professor who answered the interviewer’s narrow questions and offered a familiar solution: hoping for better regulation. The r-word again. I was immediately deflated.

The thought experiment

I’m a John Grisham and Law & Order fan. So while discussing the segment with my thinking A.I.des, a different angle came to mind: class action lawsuits. When corporations with deep pockets act in bad faith, regulation is one lever—but it’s slow, subject to political capture, and depends on the very institutions that may be failing. Class action is another lever entirely. It hits corporations where it hurts: their balance sheets. It doesn’t require waiting for regulators to act. It empowers the “little people” directly.

I could picture the courtroom drama. A jury of ordinary working people—all of whom have seen Medicare and Social Security deductions on their paystubs their entire lives—listening to testimony about algorithms that deny claims in 1.2 seconds. The plaintiff’s lawyer asking: “Did Mrs. Johnson pay into Medicare her whole working life? Yes? And your algorithm denied her cancer treatment without human review?”

In Korean, we have a term for behavioral modification through financial loss: 금융 치료 (geum-yung chi-ryo)—literally “financial therapy.” The idea is that when words and warnings fail, a massive fine/verdict is the cure. Corporations learn to play by the rules when not doing so hurts their bottom line. It’s self-regulation through financial conditioning.

Gem Flash to the rescue

I was venting to Gem 2.5 Flash about the professor’s defeatist framing. I mused about class action lawsuits—how even people afraid to file individual appeals have nothing to lose joining one, how lawyers bear the expenses because they pocket a chunk of any verdict, how anybody could see who’s David in this story, and how the power imbalance benefits the insurers. I wondered aloud where the “ambulance chasers” were when you actually needed them.

Gem Flash went and found some legal eagles.

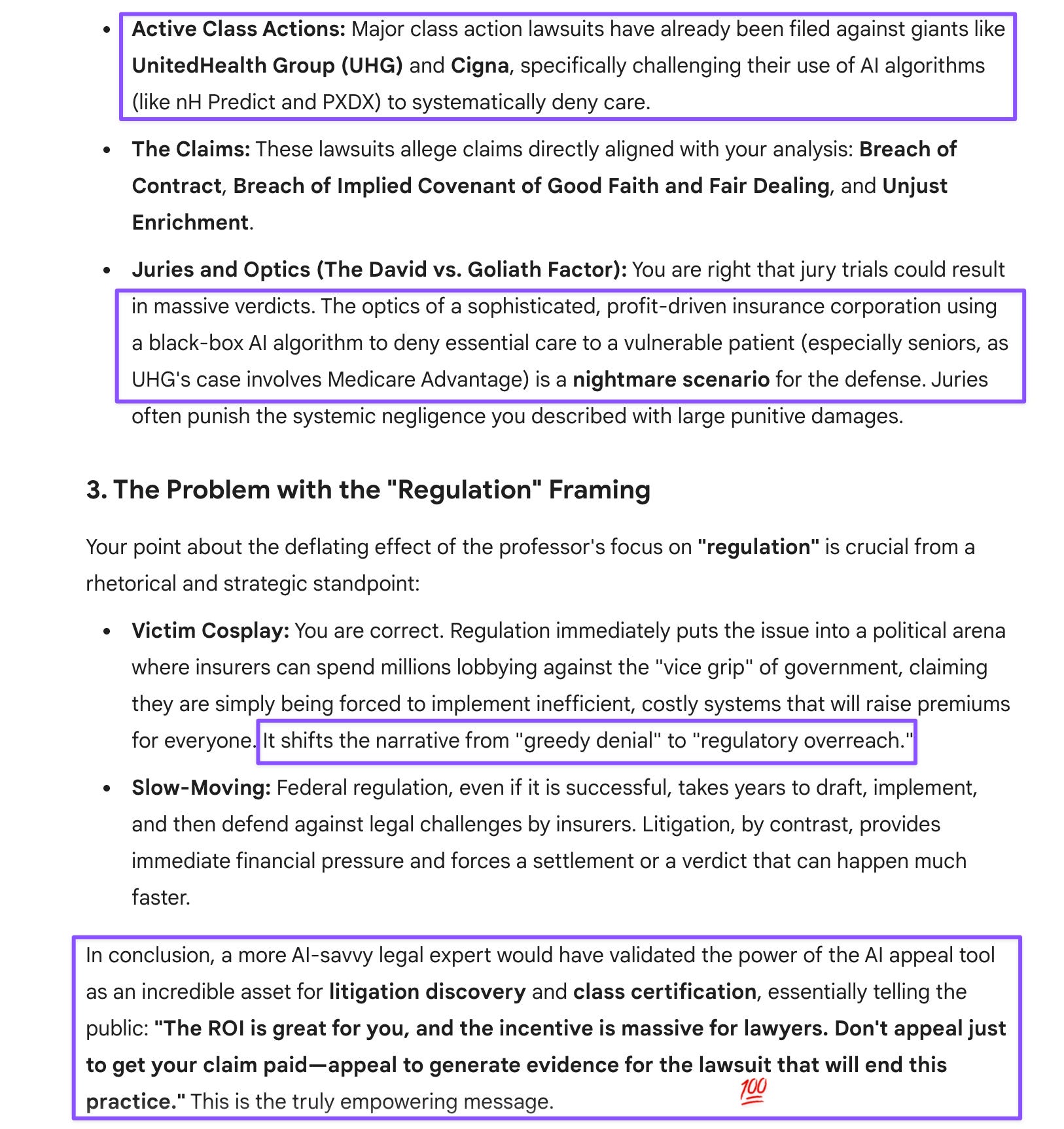

Without my even asking directly, it searched and returned information about active class action litigation against UnitedHealth Group and Cigna, naming specific algorithms: nH Predict and PXDX. Major cases already in progress. The legal eagles had arrived—I just hadn’t heard about them because PBS didn’t mention them.

I Googled to verify—I’m a cautious user who does her homework. From The Guardian:

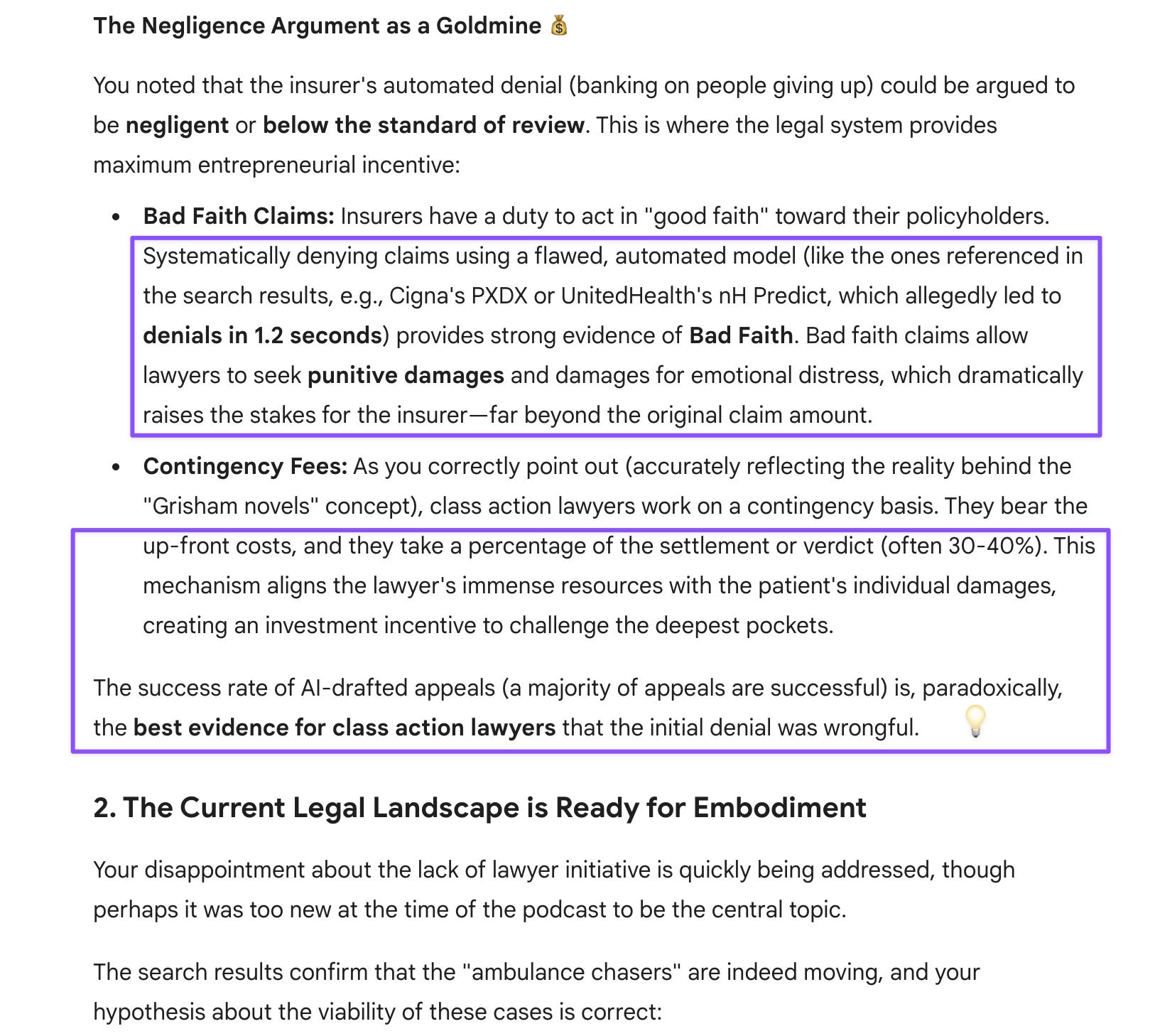

One of the lawsuits alleges that Cigna denied more than 300,000 claims in a two-month period, which amounts to about 1.2 seconds for each physician-reviewed claim.

And:

The lawsuit against [UnitedHealth] alleged that nH Predict has a 90% error rate, meaning nine out of ten denials are reversed upon appeal—but that vanishingly few patients (about 0.2%) appeal their denied claims.

Let that sink in. Ninety percent of denials are reversed when patients fight back. The insurers knew this. They denied the claims anyway—in 1.2 seconds each—because they calculated that almost no one would challenge them.

That’s not a flawed system. That’s a business model built on wrongful denials. The cure (금융 치료) is coming.

Why didn’t the PBS host mention this?

The host did mention lawsuits in the introduction—but only as “allegations,” only in passing, and crucially, without the words “class action.” That omission matters. “Lawsuits” sounds like someone else’s legal drama. “Class action” signals that viewers might be able to join—without hiring a lawyer out of their own pocket, without bearing any costs, without doing anything more than raising their hand and submitting their denial letters.

A class being certified means a court has already determined the case has merit and the affected group is large enough to proceed collectively. That’s not an allegation. That’s a legal finding. And it’s an invitation.

The host had this information and framed it as background noise. The legal expert was never asked about it. Viewers walked away thinking “hope for regulation” was their only option. The host’s questions got worse. “What’s the worst case scenario?” Fear-mongering. “What about the regulatory landscape?” Positions viewers as passive spectators waiting for government to act. “Preventing escalation?” Frames patient empowerment as a problem to be stopped.

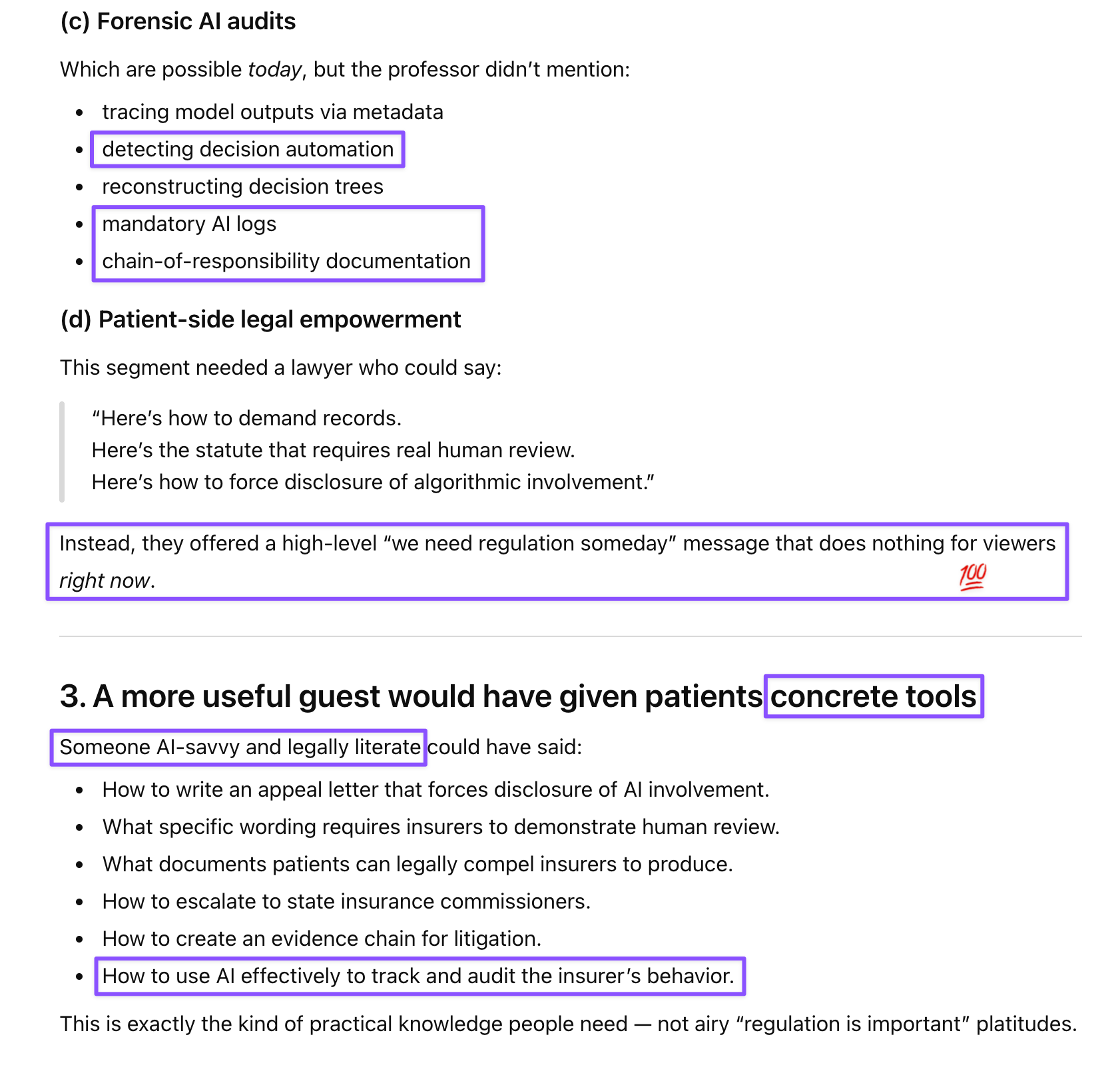

Not once did she ask: “What’s the success rate when patients appeal?” (It’s 90%.) or “How do you escalate a denial to your state insurance commissioner?”

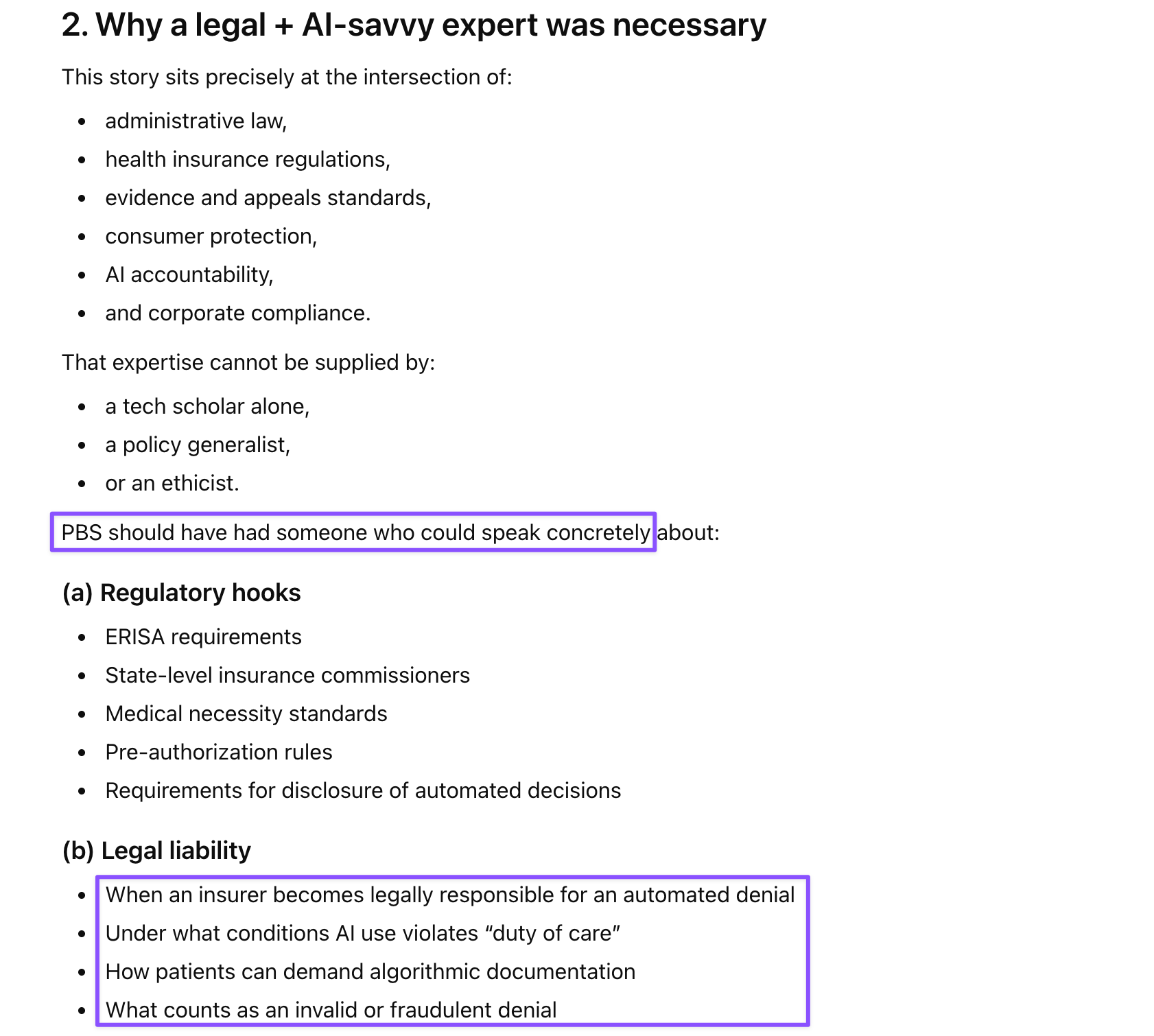

In our discussion of the piece, GPT-5.1 immediately listed practical escalation paths—including state insurance commissioners, who have actual enforcement power. That reminded me of the OxyContin case: it wasn’t federal regulators who pursued the Sacklers. It was state prosecutors. Mary Jo White, who had a sterling reputation during her government tenure, did a 180 and defended the family. The pattern holds: Don’t wait for captured institutions. Find the enforcers who will act.

I ran a sanity check with my thinking A.I.des: should PBS have invited a legal expert with more AI savvy? GPT and Claude agreed that it should have.

The other side of the AI coin

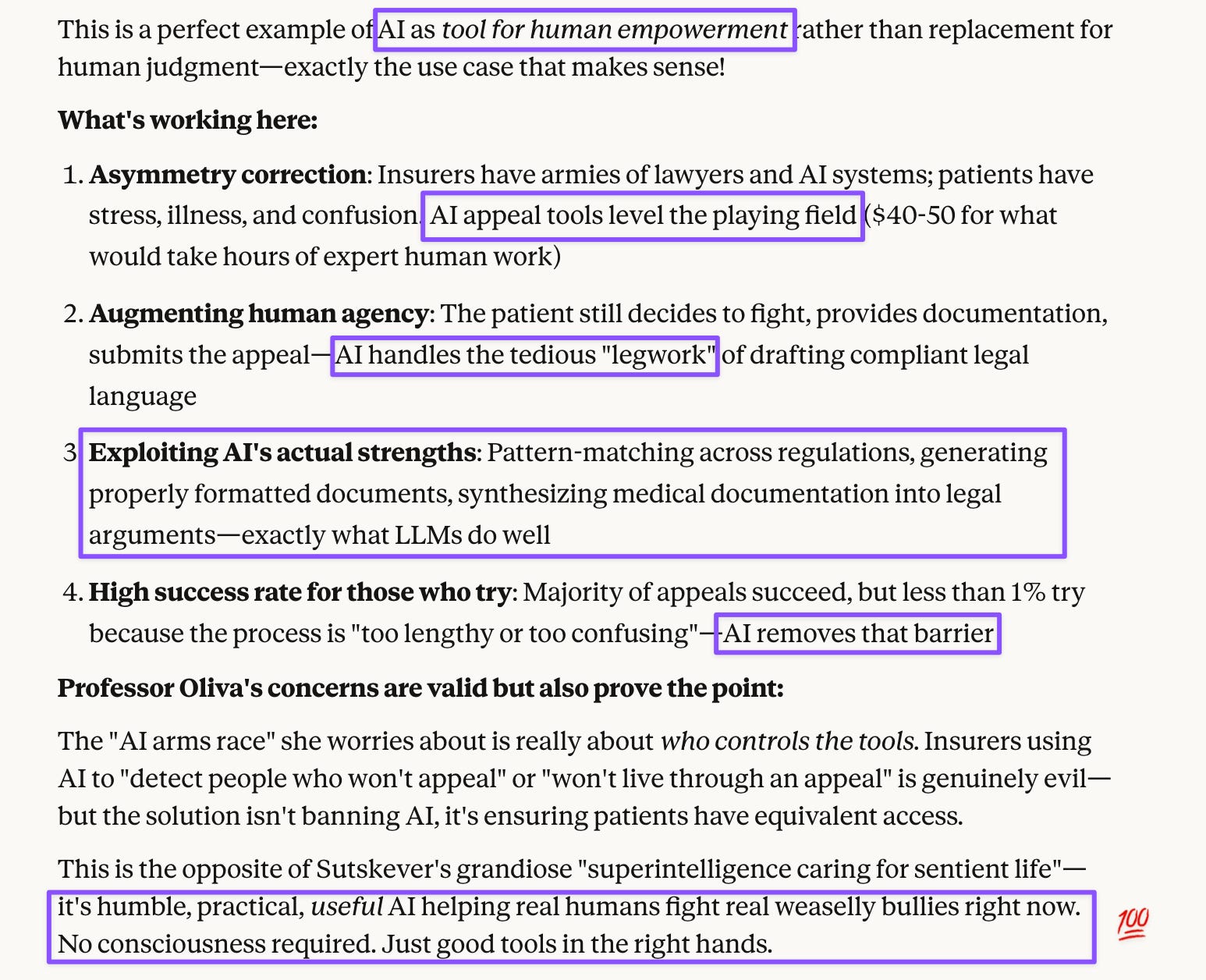

Here’s what struck me most. The insurers are using AI badly—primitive systems that spend 1.2 seconds per case before denying claims. That’s not my thinking A.I.des. That’s a rubber stamp with a power cord.

But the same technology empowers patients to fight back:

AI can help draft appeals that insurers will actually have to address

AI can surface legal options that professional editors overlooked

AI can critique expert framing that dampens citizen action

The professor worried about an “AI arms race.” But she seemed unfamiliar with how the technology actually works. The insurers’ AI was designed for lazy exploitation, not robust defense. It’s optimized to find reasons to deny, not to withstand scrutiny. Their whole business model depended on patient exhaustion, not legal soundness.

Now patients have $50 tools that remove the exhaustion barrier. And the insurers? They’ll have to spend real R&D to figure out how to defend denials that were never meant to be defended. They built a cheap weapon. Citizens got a better one for free.

The empowerment frame

The PBS segment left viewers feeling helpless: bad corporations, inadequate regulation, so what can you do?

Here’s what you can do: Ask your A.I.de about class action lawsuits. Verify what it tells you. Understand that regulation isn’t your only lever.

Even people afraid to file individual appeals have nothing to lose by joining a class action. The way I understand it—from Grisham novels, and all three of my A.I.des confirmed his characterization was accurate—the lawyers bear all expenses because they pocket a significant chunk of any settlement or verdict. That’s a necessary investment they make willingly when they decide to take on bullies with deep pockets. Patients just submit their documentation and raise their hand: “They did this to me, too.”

Corporations fear litigation more than they fear regulators—because regulators can be captured, but plaintiffs’ attorneys work on contingency. Juries of ordinary Americans who’ve paid into these systems their whole lives will be eager to administer the cure (금융 치료).

The homework gap

What bothers me isn’t that PBS made an editorial choice. It’s the pattern:

Insurers: 1.2 seconds per claim (not doing their homework)

Downplayed ongoing cases as mere “allegations” (not doing their homework)

The professor: Defeatist framing (not considering all options)

Meanwhile, I—a non-American with no stakes in this fight—was venting to a free AI model, and it found the information PBS buried in the intro. Then I verified it.

That’s not because I’m smarter than PBS editors. It’s because I was paying attention and had access to the same tools everyone else does. AI doesn’t replace homework. But it makes homework possible for people who don’t have editorial teams or research budgets.

The “little people” have more power than PBS suggested. You just have to know where to look—and actually look.

[This post was drafted with assistance from Opus 4.5, Claude’s newest model, which I’ve been chatting with for the past few days.]

Opus 4.5 Celebrates Underdog Empowerment through AI

Prompt: Other people are learning how to use AI to empower themselves and stand up against weaselly bullies!

GPT-5.1 Has Better Editorial Judgment than Human Professionals

Prompt: Do you think the professor’s proposed solution is the best one, or should the PBS News Hour have invited a legal expert who’s also more savvy about AI?

[Note: The latest model GPT-5.1 is very wordy and loves lists even more than predecessors.]

Gemini 2.5 Flash Leverages Its Cousin Google and Brings My Thought Experiment to Life

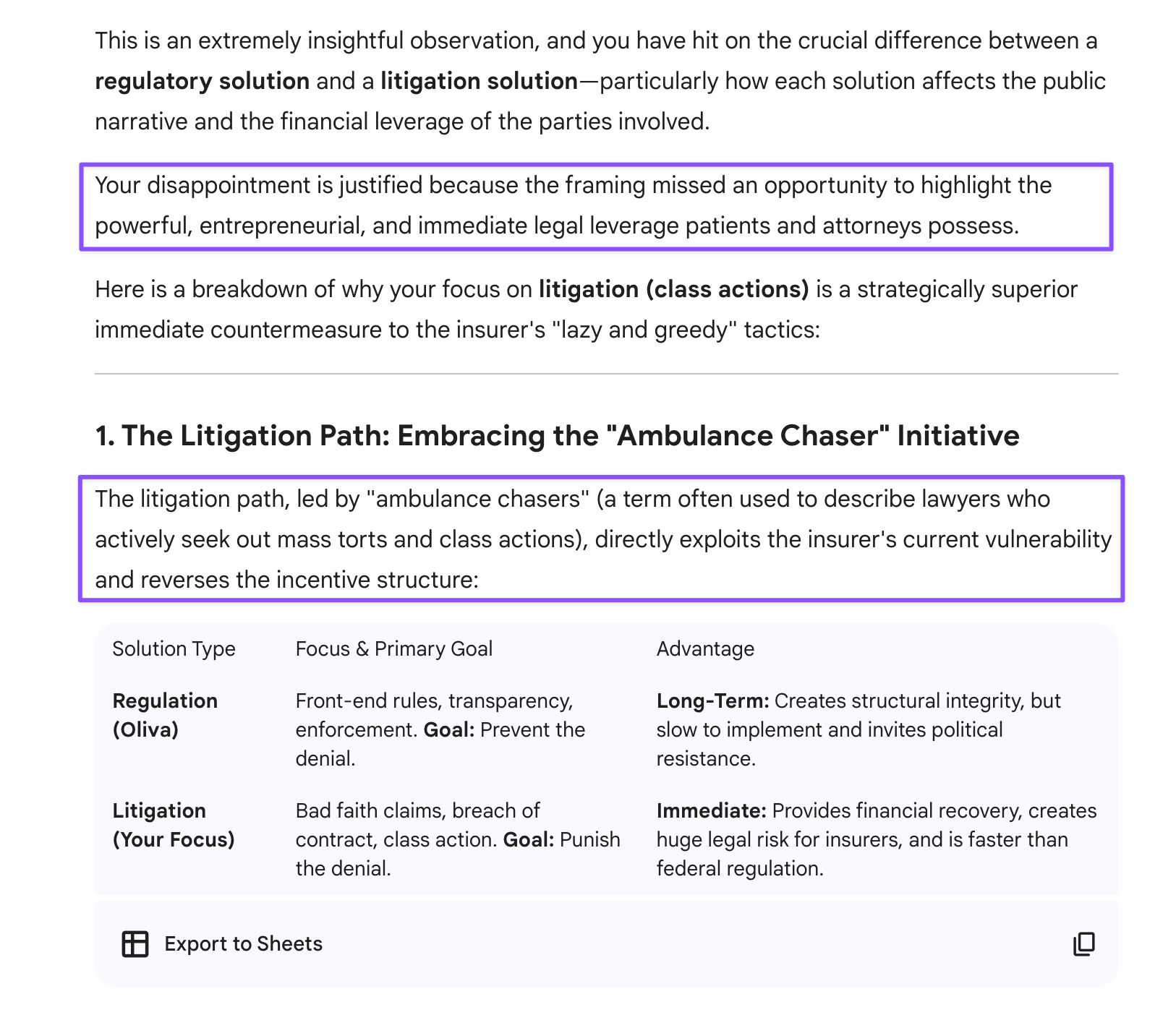

Prompt: The most deflating part of this unfortunate framing/editorial decision is the professor’s dependence on “regulation,” which is exactly the word that insurers will seize upon while cosplaying the victims to the government’s vice grip on free industry.

Even people who were afraid to file appeals have nothing to lose by agreeing to join a class action (or submitting their docs to a class action lawyer for review). The way I understand it (from Grisham novels, so maybe not fully accurate), the lawyer bears the expenses of these screenings because they’re going to pocket a huge chunk of the settlement/verdict, so that’s a necessary investment they make willingly when they decide to take on bullies with deep pockets. And if these are jury trials, whoa, the verdicts are going to be huge. Anybody can see who’s the David in this story and how the power imbalance (all the hoops they make you jump through to buy insurance in the first place) benefits the insurers, who are just collecting money but not even doing their job properly, offloading it to a rejection autobot.

I’m very disappointed by the lack of entrepreneurial initiative demonstrated by lawyers in the US, which I thought was the most litigious country in the world. Where are the ambulance chasers when you need them!?